Retirement by 58 isn’t a dream. It’s a plan – let’s build yours

The Building Blocks of Investing: A Deep Dive into Bond Basics and Portfolio Strategy

5/23/20266 min read

When most people think of investing, they often focus on the high-stakes world of the stock market. But while stocks usually steal the spotlight, bonds are the quiet engine that keeps many portfolios running smoothly.

Think of a bond as a loan in reverse. Instead of you borrowing from a bank, you act as the bank and lend money to an entity—usually a government or a corporation. In return, they promise to pay you back the full amount on a specific date, plus regular interest payments along the way.

The Anatomy of a Bond

To understand how a bond works, you only need to know four key terms:

Face Value (Par Value): The amount of money the issuer is borrowing and will pay back to you when the bond matures.

Coupon Rate: The fixed interest rate the issuer pays you (e.g., 5% on a $1,000 bond equals $50 a year).

Maturity Date: The specific date when the issuer must return your original loan.

Issuer: The entity borrowing the money. Treasury bonds are backed by the government, while Corporate bonds are issued by companies to fund growth.

Understanding Duration: The Volatility Yardstick

A common mistake is thinking a bond's price is static until it matures. In reality, bond prices fluctuate constantly based on interest rates. This sensitivity is measured by duration.

Duration is expressed in years, but it acts as a percentage multiplier for price movement. There is an inverse relationship: When interest rates go up, bond prices go down (and vice versa).

The Rule of Thumb: For every 1% change in interest rates, a bond’s price will move in the opposite direction by approximately 1% for every year of duration.

Duration in Action:

The 5-Year Bond: If you hold a bond with a 5-year duration and interest rates drop by 1%, the bond’s price will roughly increase by 5%. If rates rise by 1%, the price would fall by roughly 5%.

The 20-Year Bond: Long-term bonds are much more sensitive. A 1% rise in rates could lead to a 20% drop in value.

The 2022 Reality Check: We saw this play out vividly in 2022. As the Federal Reserve aggressively hiked rates to combat inflation, long-term Treasury bonds saw price declines of over 25-30%. This was a rare year where the "safety" of long-term bonds evaporated, causing them to drop just as sharply as—or even more than—the S&P 500.

The Power of the "Short End": SGOV and Cash Equivalents

Because of the volatility seen in 2022, many investors have shifted their focus to the "short end" of the curve. Short-term bonds have very low duration, meaning their prices stay extremely stable even when interest rates are jumping around.

Example: SGOV (iShares 0-3 Month Treasury Bond ETF)

An ETF like SGOV invests in U.S. Treasury bills with maturities of three months or less.

Duration: Practically zero.

Benefit: It behaves almost like a high-yield savings account but is backed by the full faith and credit of the U.S. government. When rates rise, SGOV doesn't lose significant value; instead, it simply starts paying a higher yield relatively quickly.

The Warren Buffett "90/10" Strategy

Even one of the world’s greatest stock pickers, Warren Buffett, believes in the power of simple bond basics. In his instructions for his wife’s inheritance, he famously suggested:

90% in a low-cost S&P 500 index fund.

10% in short-term government bonds.

By keeping that 10% in short-term debt (rather than long-term bonds), the portfolio avoids the massive price swings of duration risk. This 10% acts as a "liquid reserve" that maintains its value even during a market crash, providing peace of mind and dry powder if needed.

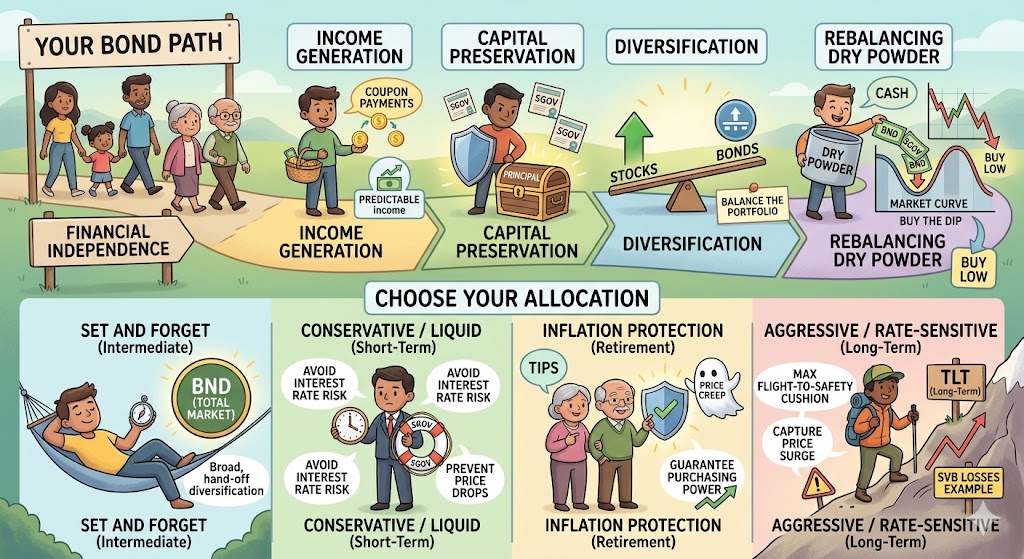

Why Put Bonds in Your Portfolio?

If stocks are for growth, bonds are for stability and income. They serve four primary roles:

Income Generation: Bonds provide a predictable stream of "coupon" payments.

Capital Preservation: Short-term bonds (like SGOV) are excellent for keeping your principal safe.

Diversification: Historically, bonds balance out your total portfolio value, though as 2022 showed, duration management is key to making this work.

Rebalancing Dry Powder: When the stock market takes a dip, bonds act as an accessible store of value. You can sell a portion of your stable bond sleeve to buy equities at a discount, automatically executing a "buy low" strategy.

How to Choose Your Allocation

A classic starting point is the "110 minus your age" rule: subtract your age from 110 to determine your stock percentage, and put the rest in bonds. For example, at age 40, you might hold 70% stocks and 30% bonds.

When selecting those bonds, consider your strategy and risk tolerance:

Set and Forget (Intermediate): Use a total market fund like BND (Vanguard Total Bond Market ETF). It covers the entire investment-grade U.S. bond market, providing broad, hands-off diversification in a single fund with moderate interest-rate sensitivity.

Conservative / Liquid Cash (Short-Term): Use short-term Treasury ETFs like SGOV or BIL for your bond sleeve to completely avoid interest rate risk, lock in current yields, and prevent any principal price drops.

Inflation Protection (Retirement Focus): Incorporate TIPS (Treasury Inflation-Protected Securities). These are essential for capital preservation during the distribution phase, as their principal adjusts with CPI to guarantee your purchasing power isn't eroded by inflation.

Aggressive / Rate-Sensitive (Long-Term): Use long-term bonds (like TLT). While highly volatile, they are a reasonable choice if you want the maximum "flight-to-safety" cushion during a stock market crash, or if you want to lock in long-term yields because you expect interest rates to fall.

⚠️ The Silicon Valley Bank Lesson on Long-Term Bonds

Think long-term government bonds are entirely risk-free because they are backed by the U.S. Treasury? Look no further than the collapse of Silicon Valley Bank (SVB) in 2023.

SVB loaded up on long-term fixed-rate bonds when interest rates were near zero. When the Federal Reserve rapidly raised rates to fight inflation, the market value of those long-term bonds plummeted (just like TLT did). When depositors unexpectedly asked for their cash back, SVB was forced to sell those bonds early, locking in a fatal $1.8 billion realized loss that triggered a catastrophic bank run.

The Takeaway: The U.S. government will always pay your principal back at maturity, but if you have to sell a long-term bond early during a rising rate environment, your paper losses become permanent realities. Never back into long-term duration if you might need that cash in the near future.

The Bottom Line

Bonds are rarely the stars of dinner party financial conversations, but they provide the essential balance needed for long-term financial health. If stocks are the engine of your portfolio, bonds are the brakes and the suspension—they ensure that your portfolio doesn't just grow, but actually survives the inevitable economic storms along the way.

It is easy to look at recent history and feel skeptical. But it is vital to understand that the 2022 bond crash was a historic anomaly, not the norm. In fact, it was the worst year for the U.S. bond market in over a century, driven by an unprecedentedly fast pivot from near-zero interest rates to fight sudden inflation. Historically, bonds have a remarkably consistent track record of moving inversely to stocks during a crisis.

Because of that historical consistency, the greatest, unsung benefit of a solid bond allocation is psychological insurance. When the stock market goes into a freefall, looking at your account and seeing a stable, income-generating bond sleeve provides the emotional buffer needed to keep you calm. It prevents the panic-selling that destroys long-term wealth, giving you the confidence to stay the course and remain fully invested when everyone else is fleeing.

Ultimately, successful bond investing comes down to intent and alignment:

Absolute Safety & Liquidity: If you need a rebalancing fund or cash for upcoming short-term expenses, anchor yourself to short-term Treasury funds like SGOV or BIL.

A Broad-Market Cushion: If you want a hands-off, total-market foundation, let a fund like BND handle the heavy lifting.

Inflation Protection: If you are approaching the distribution phase and need to lock in purchasing power against rising living costs, insulate your retirement with TIPS.

Max Growth Hedge: If you choose to venture into long-term duration like TLT, ensure you have the timeline to outlast interest rate volatility so you never find yourself in a forced-selling scenario like Silicon Valley Bank.

By matching the duration of your bonds to the timeline of your financial goals, you eliminate the guesswork. You transform your fixed-income sleeve from a confusing asset class into a strategic weapon—giving you the peace of mind to let your equities compound, the dry powder to buy market dips, and the security to enjoy the journey to financial independence.